Every year, your prescription drug coverage changes - often without you noticing until you walk up to the pharmacy counter and your copay jumps from $10 to $113. If you're on Medicare Part D, or even if you get your drugs through an employer plan, you're not alone. In 2025, millions of people faced sudden shifts in what medications are covered, how much they pay, and which versions of their drugs they’re allowed to use. The big driver? Formulary updates. These aren't just paperwork tweaks. They're real, financial, and sometimes life-altering decisions made by insurance companies and pharmacy benefit managers (PBMs) that directly affect whether you can afford your medicine.

What Exactly Is a Formulary?

A formulary is a list of drugs your insurance plan will pay for. It's not a fixed document. It changes every year. Think of it like a grocery store’s sale rack: some items get promoted (lower cost), others get pulled off the shelf entirely. In 2025, the biggest changes came from the Inflation Reduction Act (IRA) of 2022. One major shift: the end of the "donut hole." Before 2025, once you spent a certain amount on drugs, you hit a gap where you paid 100% out-of-pocket. Now, that gap is gone. Between $5,030 and $8,000 in spending, you pay 25% - no matter what. That’s a win for many, but it’s not the whole story.

What’s really reshaping formularies is the push toward generics and biosimilars. These are cheaper versions of brand-name drugs. Generics are exact copies of small-molecule drugs - like metformin or lisinopril. Biosimilars are similar, but not identical, copies of complex biologic drugs - like Humira or Enbrel. PBMs like CVS Caremark, OptumRx, and Express Scripts are aggressively moving patients from expensive brands to these lower-cost alternatives. Why? Because they save money. And under the IRA, they’re now financially rewarded for doing so.

How Tiered Copays Work in 2025

Your formulary is split into tiers. Each tier has a different cost to you. In 2025, here’s what you’re likely seeing:

- Tier 1: Preferred generics - $1 to $10 copay. These are the drugs your plan wants you to use. Most common for blood pressure, diabetes, and cholesterol meds.

- Tier 2: Non-preferred generics or preferred brands - average $47. You might still get these, but you’ll pay more.

- Tier 3: Non-preferred brands - average $113. If your drug moved here, your out-of-pocket cost likely doubled or tripled.

- Specialty tier: High-cost drugs - $113 or 25% coinsurance. These include cancer treatments, autoimmune drugs, and rare disease therapies.

Here’s the catch: if your drug was on Tier 1 last year and got moved to Tier 3 this year, your monthly cost could jump from $10 to $113. That’s $1,236 more per year. For someone on a fixed income, that’s not just inconvenient - it’s dangerous.

What’s Actually Changing in 2025?

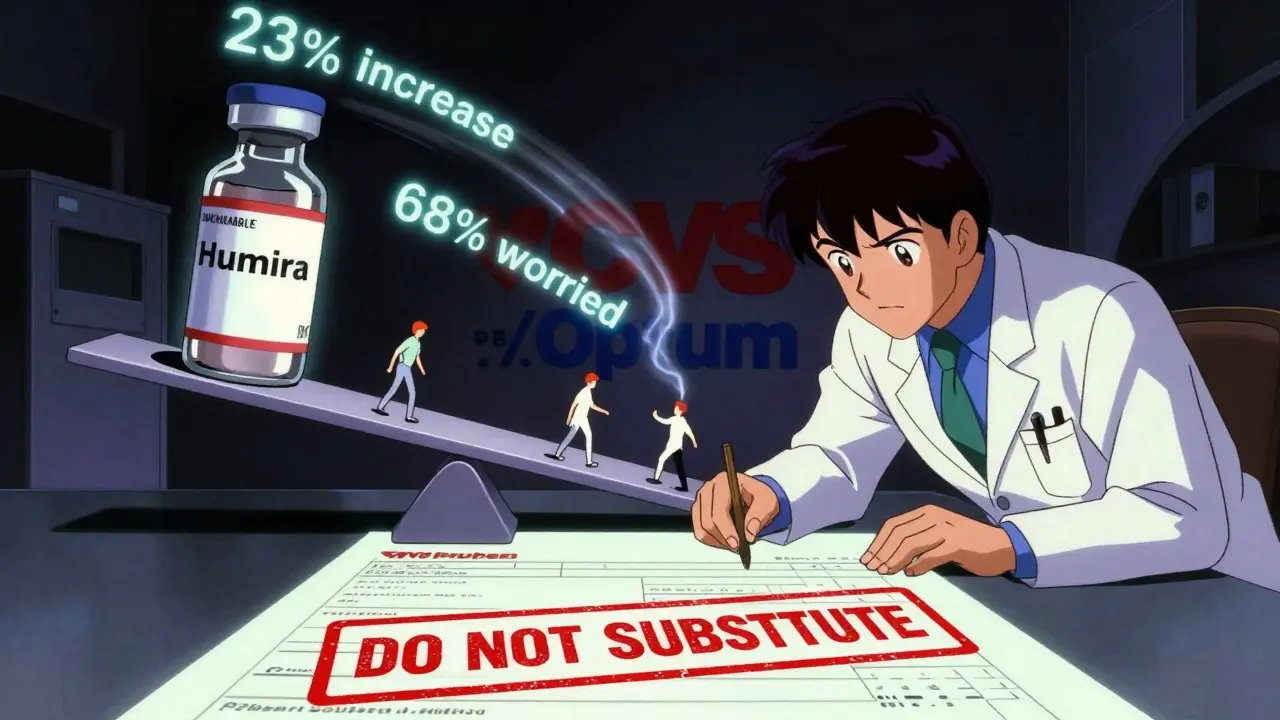

Changes aren’t random. They follow patterns. CVS Caremark’s 2025 formulary removed nine specialty drugs, including Herzuma and Ogivri (breast cancer treatments), but added 18 new ones - 11 of them biosimilars like Kanjinti and Trazimera. That’s not a coincidence. These biosimilars are proven to work the same way, but cost 30-70% less. UnitedHealthcare moved Humalog insulin to a higher tier, causing a spike in copays from $35 to $113. Meanwhile, Cigna and Anthem eliminated the donut hole entirely and lowered out-of-pocket caps.

But here’s the tension: while some patients save hundreds a month by switching to biosimilars - like one user who dropped from $450/month on Humira to $45 on Amjevita - others report serious disruptions. A Reddit user in r/Medicare described a switch from Enbrel to a biosimilar that caused severe flare-ups. Another person on HealthUnlocked said their diabetes meds were switched without warning, leading to uncontrolled blood sugar. These aren’t rare cases. According to data from Medicare.gov forums, 68% of respondents were worried about formulary changes affecting their meds. And 42% of those specifically feared changes to their diabetes or heart medications.

Why Generic Switching Isn’t Always Safe

It’s easy to think: "If it’s cheaper and approved by the FDA, why not switch?" But drugs aren’t like lightbulbs. A biosimilar might be "highly similar," but it’s not identical. For chronic conditions like rheumatoid arthritis, multiple sclerosis, or Crohn’s disease, even small differences in how a drug is absorbed can lead to loss of symptom control. Dr. Karen Ignagni, former CEO of America’s Health Insurance Plans, warned that "over-aggressive generic substitution could disrupt chronic disease management for vulnerable populations." That’s not fear-mongering - it’s clinical reality.

Non-medical switching - when your insurer changes your drug for cost reasons, not because your doctor recommends it - rose 23% in 2024. That’s a red flag. If your doctor wrote "do not substitute" on your prescription, insurers are supposed to honor that. But many don’t. And even when they do, the process can take weeks. Cigna’s own data shows 38% of patients waited 10 to 14 days for an exception approval. That means running out of meds. That means ER visits. That means worsening health.

What You Can Do: 5 Practical Steps

You don’t have to wait for a surprise bill. Here’s how to take control:

- Review your formulary between October and December. Every insurer sends a notice by mail or online. Don’t ignore it. Look up your exact drug name - not just the brand, but the generic too.

- Ask your pharmacist. Pharmacists see these changes daily. They can tell you if your drug was moved, if a biosimilar is available, or if there’s a cheaper alternative you haven’t considered.

- Check your tier. If your drug moved from Tier 1 to Tier 3, ask your doctor if there’s another drug in the same class that’s still on Tier 1. Sometimes, switching to a different medication in the same family can save you hundreds.

- Request an exception. If your drug was removed or moved to a higher tier, your doctor can file a formal exception request. In 2024, 82.3% of tiering exceptions were approved. For drugs completely removed? Only 47.1% got approved - but it’s still worth trying.

- Know your rights. Insurers must give you 60 days’ notice before changing a drug you’re already taking. If you get a new prescription, they only need 30 days. If you get a surprise change, call your plan immediately. You may be entitled to a 30-day transitional supply.

The Bigger Picture: What’s Coming in 2026

2025 was just the beginning. In January 2026, a new rule kicks in: the Medicare Drug Price Negotiation Program (MDPNP). For the first time ever, the government will negotiate prices for 10 high-cost drugs - including Stelara, Prolia, and Xolair. Insurers will be required to cover them at those negotiated prices. That means biosimilars for these drugs will hit the market in early 2026, and insurers will likely push them hard.

By 2027, experts predict biosimilar use in targeted therapies could reach 45%, up from 28% in 2024. That’s huge. But it also means more pressure on patients to switch. And if you’re on one of those 10 negotiated drugs, you’ll have no choice - your plan will cover only the negotiated version.

What’s clear is this: insurance companies are no longer just managing risk. They’re managing cost. And they’re using formularies as their main tool. The goal isn’t to hurt patients - it’s to reduce spending. But without oversight, that goal can become a trap.

Final Thought: Your Medication Isn’t a Line Item

It’s easy to think of your prescription as just another cost. But for someone with diabetes, heart disease, or an autoimmune disorder, that pill is what keeps them alive, mobile, and independent. The system is changing - faster than ever. And if you’re not paying attention, you could be left paying more, waiting longer, or taking a drug that doesn’t work for you.

The good news? You have power. You can ask questions. You can request exceptions. You can push back. You can talk to your pharmacist, your doctor, and your insurer. You’re not powerless. You just need to know what’s coming - and act before January 1.

What happens if my drug is removed from the formulary entirely?

If your drug is removed, your insurer must give you at least 60 days’ notice if you’re already taking it. You can ask your doctor to file a formal exception request. If approved, you’ll continue to get the drug at your current cost. If denied, you may be able to get a 30-day transitional supply while you switch. For drugs completely removed, only about half of exception requests are approved - so act fast.

Can I be forced to switch to a biosimilar?

Insurers can require you to try a biosimilar first (step therapy), but they can’t force you to switch if your doctor says it’s medically inappropriate. If your doctor writes "do not substitute" on the prescription, the pharmacy is legally required to honor that. However, many plans still try to override this. If that happens, file an exception immediately - and keep records of all communications.

How do I know if a biosimilar is right for me?

Talk to your doctor. Biosimilars are rigorously tested and approved by the FDA. For many people, they work just as well as the original drug - and save hundreds a month. But for those with unstable conditions (like uncontrolled RA or Crohn’s), switching can cause flare-ups. Ask your doctor: "Has this biosimilar been used successfully in patients like me?" Look for real-world data, not just marketing claims.

What if I can’t afford my new copay?

You have options. First, ask your doctor if there’s a cheaper alternative in the same class. Second, check if the drug manufacturer offers a patient assistance program - many do. Third, apply for Extra Help (Low-Income Subsidy) through Medicare. It can reduce your monthly premiums and copays by up to 90%. Finally, contact your insurer’s patient advocacy office - they often have emergency funds or payment plans.

When should I start checking for formulary changes?

Start in October. That’s when insurers begin sending out notices for changes effective January 1. Don’t wait until December. Use that time to review your current list, compare it to next year’s, and talk to your pharmacist. If you’re on a chronic medication, consider switching to a generic or biosimilar now - before the change hits. It’s easier to adjust when you’re in control.

Comments (13)

Milad Jawabra March 4 2026

This is why I tell everyone: check your formulary in October. No excuses. I got hit with a $113 copay last year for my RA med, and I almost skipped doses. I called my pharmacist, they found a biosimilar that worked, and now I pay $45. It’s not magic - it’s vigilance. 🤞Sharon Lammas March 5 2026

There’s something deeply unsettling about treating life-sustaining medication like a commodity on a balance sheet. The system doesn’t care if you’re stable - only if you’re cheap.Diane Croft March 5 2026

You’re not alone. I’ve been there. And I’m here to say - you’ve got options. Ask. Push. File. You’re stronger than the formulary.Tildi Fletes March 6 2026

The Inflation Reduction Act's formulary provisions represent a structural recalibration of pharmaceutical cost allocation. While the elimination of the donut hole is statistically significant, the aggressive tiering of biosimilars introduces a latent risk of therapeutic discontinuity, particularly among patients with complex polypharmacy regimens.Siri Elena March 8 2026

Oh wow, a 1000-word essay on how insurance companies are evil. Shocking. I thought they were just trying to not go bankrupt while you all keep ordering $12,000/month biologics like they’re Starbucks lattes.Divya Mallick March 8 2026

This is the consequence of Western medical capitalism. In India, we have Ayushman Bharat - universal coverage. No tiered copays. No biosimilar coercion. Just access. You think your $113 copay is bad? Try paying 80% of your monthly income for insulin. We don’t have PBMs. We have people.Pankaj Gupta March 8 2026

The data is clear: biosimilars reduce costs without compromising outcomes. Studies show non-inferiority in 92% of cases. The fear-mongering about "small differences" ignores clinical evidence. If your doctor hasn’t reviewed the literature, they’re not doing their job.Chris Beckman March 9 2026

i read this whole thing and like... why are people so mad? it's just money. if you can't afford your meds, go to a free clinic. or ask for help. or get a second job. stop blaming the system. it's not broken - you're just not trying hard enough.Richard Elric5111 March 9 2026

The ontological dilemma of pharmaceutical policy lies in the tension between utilitarian cost-efficiency and deontological patient autonomy. When a PBM replaces a biologic with a biosimilar without clinical consultation, it transgresses the Kantian imperative of treating persons as ends, not means.Dean Jones March 11 2026

I’ve been on Humira since 2018. Switched to Amjevita last year because my plan forced it. At first, I thought, "cool, I’ll save $400." Then my knees started locking up again. My rheumatologist said it was a classic case of immunogenicity from the biosimilar. Took 8 weeks to get my original back. I missed work. My dog stopped cuddling with me because I was in pain all the time. This isn’t about savings. It’s about trust. And the system broke mine.Betsy Silverman March 11 2026

I’m a pharmacy tech. I see this every day. People cry in the aisle because their copay jumped. We can’t override it. We can’t change it. All we can do is hand them a pamphlet and say, "Call your doctor. File an exception. You’ve got rights." So thank you for writing this. Someone needs to say it.Ivan Viktor March 13 2026

So what you’re saying is… we’re all just rats in a maze, and the cheese is now $113 a pill? Yeah, I get it. I’ve been there. I’m just glad I don’t have kids who need this stuff. Cheers.Matt Alexander March 14 2026

Just check your formulary in October. Talk to your pharmacist. Ask for the generic. If it’s moved, ask your doctor for another drug in the same class. Done. No drama.